Dom's notes

Despite having been hammered for posting my sincere feedback re. ATW in the appropriate thread (or may-be, because of ...) I am starting this thread for the benefit of all waanabee traders.

I have no intent of sharing my exact trade setups, however I will share as much as I can - the good, the bad & the ugly, and if someone learn something from this then it won't have been a waste of my time.

I have been a student of the market for over 4 years now. I actually started my education with Investools PhD program (which was a lot of money for not much outcome in my case), trading stocks then options, then started to focus on the SPX (directional Calls/Puts then credit spreads), at some point I discovered the futures / ES in particular and that was a "revelation" ... 1/4pt spread vs 2pt spread for the SPX options, I was sold in no-time.

I purchased Todd Mitchell's system (TradingConcepts), which was a lot less money than Investools but no more outcome in my case, at least it triggered my interest in Fibs (back then, retracements only) and I did a lot of research / backtesting using Fibs - but at the end of the day, the real challenge resides in figuring out which fib level will "hold", and to this day I have to admit I have not solved it.

Anyway, I then spent a lot of time in a couple of "free" trading rooms

learning pure price action, the person that was offering his time teaching PA free for several months later offered a paying program, which I took, but I still couldn't make money live. I took another mentor, recommended on a free forum, and despite he being a nice guy (and why wouldn't he be when students are paying), this also was a failure.

I was about to throw the towel when I found ATW, started with the 101A education, added 3 weeks later the mentorship education, and have been studying / backtesting a lot for now a full year. I reached a point where I can "consistently" make fake-money on sim, however the transition to live trading is a real challenge for me, because of fear I pass on many trade setups and I deviate from my trade management rules.

So, that's the background. I trade CL (Crude Oil "big" contract) which is very liquid, has 1 tick spread throughout the European & US session, and is nicely volatile (day range is on average 250-350 ticks, some days even more - like today : 450 ticks). I find CL to have a lot of momentum, it shows very repetitive "patterns" (at least, for the fib user that I am).

I don't use any indicator, I trade price action using a lot of price projection techniques (best book IMO on this topic is Robert C. Miner "Dynamic Trading").

If I have one advice for new traders, it is look for another way of making a living ... but if you are truly in love with the markets, then I believe it is a must to 1) find an excellent education (this is way more than just reading books, and frankly, there is probably no one-stop education shop) and 2) find a mentor to accelerate your learning curve.

Now that this is out of the way, a brief summary of my week :

Tuesday - tried 1 trade early morning, entry hit no fill, that made me mentally sick for the rest of the day, I passed on 2 setups (both wins), the last setup I tried but my entry wasn't even close to be hit.

Wednesday - 2 setups no-fill, then 1 small winner (got out at 1/2 of my target for pseudo-good reasons - really, lack of discipline), and I passed on the last one (another wouldabe winner :( )

Thursday - passed on 5 setups (4 wins / 1 loss), took 1 small winner (1/2 target again, same lack of discipline), and missed the best setup of the day by being away for 5min

Friday - passed on 1 setup (win), no fill on next 2 setups, then I couldn't focus & called it a day.

Bottom-line - only 2 trades this week, I made ~10% of what I should have made if I had the discipline to follow my plan.

I have no intent of sharing my exact trade setups, however I will share as much as I can - the good, the bad & the ugly, and if someone learn something from this then it won't have been a waste of my time.

I have been a student of the market for over 4 years now. I actually started my education with Investools PhD program (which was a lot of money for not much outcome in my case), trading stocks then options, then started to focus on the SPX (directional Calls/Puts then credit spreads), at some point I discovered the futures / ES in particular and that was a "revelation" ... 1/4pt spread vs 2pt spread for the SPX options, I was sold in no-time.

I purchased Todd Mitchell's system (TradingConcepts), which was a lot less money than Investools but no more outcome in my case, at least it triggered my interest in Fibs (back then, retracements only) and I did a lot of research / backtesting using Fibs - but at the end of the day, the real challenge resides in figuring out which fib level will "hold", and to this day I have to admit I have not solved it.

Anyway, I then spent a lot of time in a couple of "free" trading rooms

learning pure price action, the person that was offering his time teaching PA free for several months later offered a paying program, which I took, but I still couldn't make money live. I took another mentor, recommended on a free forum, and despite he being a nice guy (and why wouldn't he be when students are paying), this also was a failure.

I was about to throw the towel when I found ATW, started with the 101A education, added 3 weeks later the mentorship education, and have been studying / backtesting a lot for now a full year. I reached a point where I can "consistently" make fake-money on sim, however the transition to live trading is a real challenge for me, because of fear I pass on many trade setups and I deviate from my trade management rules.

So, that's the background. I trade CL (Crude Oil "big" contract) which is very liquid, has 1 tick spread throughout the European & US session, and is nicely volatile (day range is on average 250-350 ticks, some days even more - like today : 450 ticks). I find CL to have a lot of momentum, it shows very repetitive "patterns" (at least, for the fib user that I am).

I don't use any indicator, I trade price action using a lot of price projection techniques (best book IMO on this topic is Robert C. Miner "Dynamic Trading").

If I have one advice for new traders, it is look for another way of making a living ... but if you are truly in love with the markets, then I believe it is a must to 1) find an excellent education (this is way more than just reading books, and frankly, there is probably no one-stop education shop) and 2) find a mentor to accelerate your learning curve.

Now that this is out of the way, a brief summary of my week :

Tuesday - tried 1 trade early morning, entry hit no fill, that made me mentally sick for the rest of the day, I passed on 2 setups (both wins), the last setup I tried but my entry wasn't even close to be hit.

Wednesday - 2 setups no-fill, then 1 small winner (got out at 1/2 of my target for pseudo-good reasons - really, lack of discipline), and I passed on the last one (another wouldabe winner :( )

Thursday - passed on 5 setups (4 wins / 1 loss), took 1 small winner (1/2 target again, same lack of discipline), and missed the best setup of the day by being away for 5min

Friday - passed on 1 setup (win), no fill on next 2 setups, then I couldn't focus & called it a day.

Bottom-line - only 2 trades this week, I made ~10% of what I should have made if I had the discipline to follow my plan.

CL Always-In : 2 wins / 6 losses / 2 ~BE ; net -1280

It was the 6th consecutive losing week. Really not fun.

I have my first client trading live since yesterday (1 win / 1 loss ; ~ +500), I wish him the best! Interestingly, problems started almost right away, actually during the session-break yesterday, as the order-feed went down for a couple of minutes, which triggered a reload/restart, during which the strategy cancels its catastrophic stop (when it stops) & replaces it with a new one (when it restarts) - but, the FCM Gateway doesn't allow any order (new/change/cancel) when the "market is closed", so both the Cancel & the replacement order were rejected, then Ninja didn't let the strategy restart because of "unmapped orders", I had to stop Ninja, restart it, to be finally able to cancel the prior order, and restart the strategy w/o any catastrophic stop for the time being.

So, the R&D du-jour was about implementing simulated stops (& targets), which I managed to do in a very non-intrusive manner, as I have 400 lines of standalone code, + only 2 lines inserted in the existing one (1 in OnBarUpdate(), 1 in OnOrderUpdate()). Finished all testing (backtesting + real-time on MarketReplay, including rollovers & reload/restart) and deployed in the afternoon. I did not find a single bug in what I did today, but I found one from way before, using a combination of different types of stops not available in the official version of the system.

Prior to that, I spent about a day on security concerns for the VPS, in the end turning NLA on did immediately shut down almost all attacks.

Add to this a couple days of contract work, and this is a pretty good summary of my week.

Have a great week-end!

PS - I am not a fan of the white background of the new interface for this website. What is it with white? It is very aggressive, IMO.

It was the 6th consecutive losing week. Really not fun.

I have my first client trading live since yesterday (1 win / 1 loss ; ~ +500), I wish him the best! Interestingly, problems started almost right away, actually during the session-break yesterday, as the order-feed went down for a couple of minutes, which triggered a reload/restart, during which the strategy cancels its catastrophic stop (when it stops) & replaces it with a new one (when it restarts) - but, the FCM Gateway doesn't allow any order (new/change/cancel) when the "market is closed", so both the Cancel & the replacement order were rejected, then Ninja didn't let the strategy restart because of "unmapped orders", I had to stop Ninja, restart it, to be finally able to cancel the prior order, and restart the strategy w/o any catastrophic stop for the time being.

So, the R&D du-jour was about implementing simulated stops (& targets), which I managed to do in a very non-intrusive manner, as I have 400 lines of standalone code, + only 2 lines inserted in the existing one (1 in OnBarUpdate(), 1 in OnOrderUpdate()). Finished all testing (backtesting + real-time on MarketReplay, including rollovers & reload/restart) and deployed in the afternoon. I did not find a single bug in what I did today, but I found one from way before, using a combination of different types of stops not available in the official version of the system.

Prior to that, I spent about a day on security concerns for the VPS, in the end turning NLA on did immediately shut down almost all attacks.

Add to this a couple days of contract work, and this is a pretty good summary of my week.

Have a great week-end!

PS - I am not a fan of the white background of the new interface for this website. What is it with white? It is very aggressive, IMO.

CL AlwaysIn: 9 wins / 4 losses ; net -385.

At least the win% this week is back above its long-term average. The system was caught long overnight Monday, resulting in a -2500 loss.

CL has had an abundance of abrupt overnight moves lately, where overnight in general has a statistical bias towards chop, and the system is clearly suffering from that current state of affairs. Using stops would have clearly benefited 2013 so far, despite being consistently inferior in backtest. I am almost at the decision point to turn stops on, at least overnight (working on it right now).

I have 3 more live clients this week. My fills are potentially impacted, this is a very rare week where overall I didn't get any positive slippage vs backtest. 2 of those clients had 10-ticks positive slippage for the week, it seems their execution through ZenFire is doing better than mine through IB.

Have a great week-end!

The last 2 weeks have been more of the same for my system CL AlwaysIn:

- 5 wins / 9 losses ; net -520 for the week ending 9/20

- 6 wins / 8 losses / 1 BE ; net -1925 for the week ending 9/27

If I didn't have 6.5 years of positive results for this system in backtest (6 years) and forward test (0.5 year) I would have already reversed the buy/sell signals...

Lots of contract R&D for the last 2 weeks, some of it not so fun as I am juggling with 6 markets, each 10 years history, on a 1min main timeframe, and I was working on adding a 1sec timeframe to allow for intrabar updates of the underlying model. Starting off the most complex system I have ever worked on, of course. I am half-way through that, currently using the 1min bars as only (simulated) 1sec bars, and now having both versions of the software provide identical results. To give you some idea, the 1min + 1sec simulated version can generate over 1,000,000 lines of detailed log per market on 10 year backtest.

That led me to find yet another interesting Ninja bug ... when using a 1sec TF (and only that particular TF), the 1st bar of the "RolloverTo" session is incorrectly backadjusted, leading to fairly big jumps on the 1sec TF. Of course, that bug is acknowledged by Ninja, and won't be fixed in NT7. The only way around it is to either use simulated orders on the 1sec TF, ignoring those 1sec bars, or just use a 2sec TF instead (which doesn't go without other issues, as the 1sec TF has its timestamps "bar-starting", so all 1sec bars of a 1min interval are correctly scheduled by Ninja before the 1min bar, where 2sec and all other TF timestamps are "bar-ending", and Ninja schedules the last bar of a 1min interval in the order of TF#, so if the 1min is the primary TF, the last 2sec bar of a 1min bar is scheduled by Ninja *after* the 1min bar, of course this has to be manually worked-around to ensure all bars on the 2sec TF are seen before the 1min bar.

Since it is too late to wish people a great week-end, let me wish you a great week instead!

Long time no updates! I have been very busy & just couldn't get to it.

The system has had mostly losing weeks from the beginning of July, until mid-October, and my account went back to below break-even on October 15. In the process, I lost the 4 customers that had just started with the system.

Even though my system stop was not reached, I felt I would suffer more of the same if I kept trading it as is, and given the pace of losses (-12k for just the 4 weeks ending October 11) that system stop could have been hit in a couple of weeks, or less, and there was no point continuing in the same fashion.

I took a clean-sheet approach, and did the statistical analysis all over again, paying special attention to not mix variables in the patterns definition, and to not define the patterns narrowly - all in all, trying to *not* over-fit the system. The other thing that I did, was to decide on using a reasonable size stop at all times, even when the performance in backtest is about 20% lower that way - but I had learned over the past 3 months, that stops are just there to assist when the market goes out of the usual for an extended period of time.

That new version yields on the 6 years backtest only 60% of the P&L of the prior one for about the same number of trades, but it's forward testing performance on 2013 is in-line with the last 3 years (2008 & 2009 are way above the average, and 2007 well under the average), and the current drawdown only started in September, and was of lower magnitude than with any prior version (it is currently quite less than the max historical drawdown). All in all, I thought this new version had better chances of long-term success, so I decided to switch to it, which I did at 2:30am on Wednesday, October 15.

Results for the week ending October 18:

8 wins ; 7 losses ; net -55

Results for the week ending October 25:

8 wins ; 6 losses ; net -205

Results for the week ending November 1:

8 wins ; 6 losses ; net +1970

Results for the week ending November 8:

8 wins ; 2 BE ; net +2200

The re-designed system (live since October 15) has been working decently on the last 4 weeks - the results for the week of October 18 actually include a couple days of the prior version of the system, which lost -3840 in 2 days.

That version is only -440 from its P&L peak for the year.

As of the close tonight, the realized P&L since I started trading CLAlwaysIn is +6,495 (for 471 trades!), and the current drawdown is -14,635 from the P&L peak of July.

Have a great week-end

I have not posted here in a long while ... still trading CL always-in, the system has been trading water in November-December (ha!) but is making new P&L peaks each week since January, my account was up +12,415 yesterday for 560 trades since March 19th, 2013 (that's up +6,000 since the prior post on November 8).

I have a "beta" website here : dom993.bugs3.com ... domain name to change soon.

I am currently working on a new system, "CL Selective". Also based on statistical analysis of price action, but this one's goal is to trade only the best setups.

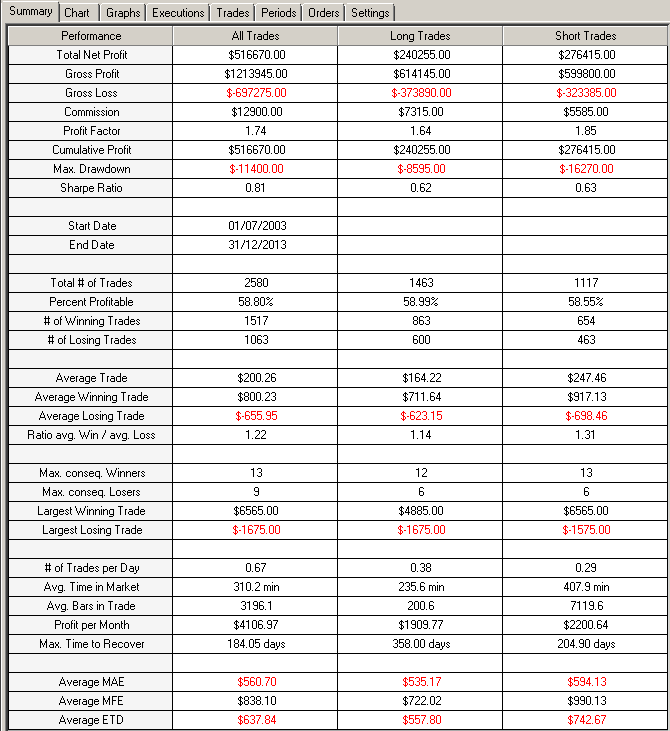

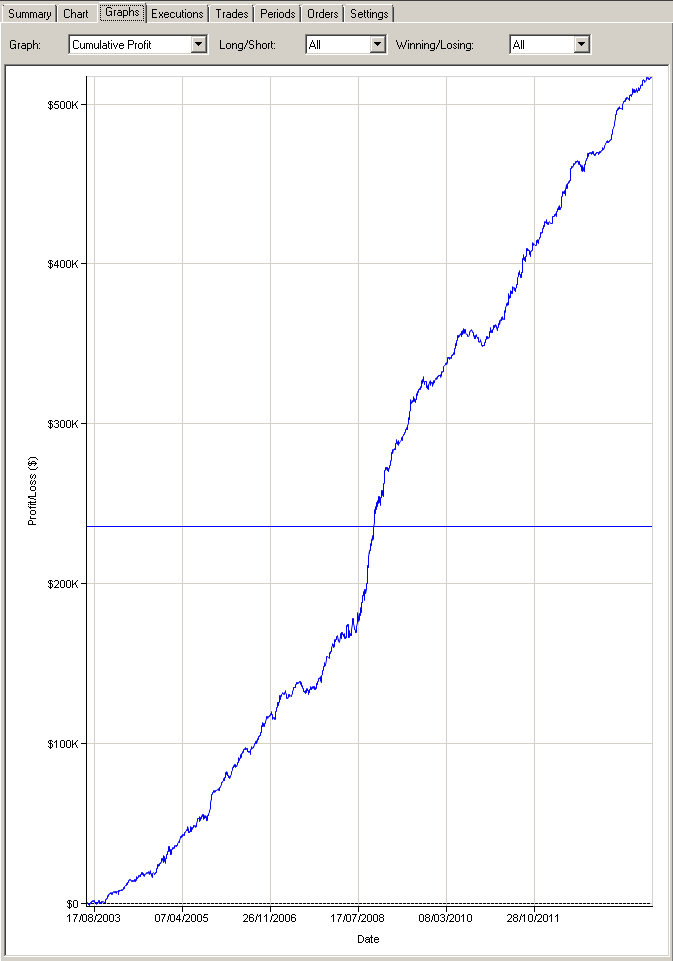

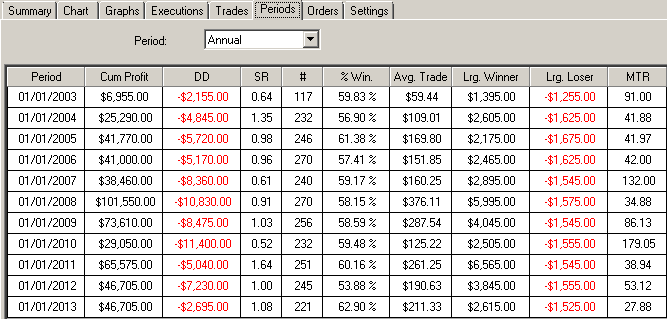

Backtested on 10.5 years of CL:

Have a great week-end!

I have a "beta" website here : dom993.bugs3.com ... domain name to change soon.

I am currently working on a new system, "CL Selective". Also based on statistical analysis of price action, but this one's goal is to trade only the best setups.

Backtested on 10.5 years of CL:

Click image for original size

Click image for original size

Click image for original size

Have a great week-end!

Dom that equity curve looks too good to be true so I'd be scared but hope it trades like that in real time....what became of your trading contest...? how did Chuck Huges do ? He wants me to spend almost 4 k on options recomendations

Emini Day Trading /

Daily Notes /

Forecast /

Economic Events /

Search /

Terms and Conditions /

Disclaimer /

Books /

Online Books /

Site Map /

Contact /

Privacy Policy /

Links /

About /

Day Trading Forum /

Investment Calculators /

Pivot Point Calculator /

Market Profile Generator /

Fibonacci Calculator /

Mailing List /

Advertise Here /

Articles /

Financial Terms /

Brokers /

Software /

Holidays /

Stock Split Calendar /

Mortgage Calculator /

Donate

Copyright © 2004-2023, MyPivots. All rights reserved.

Copyright © 2004-2023, MyPivots. All rights reserved.